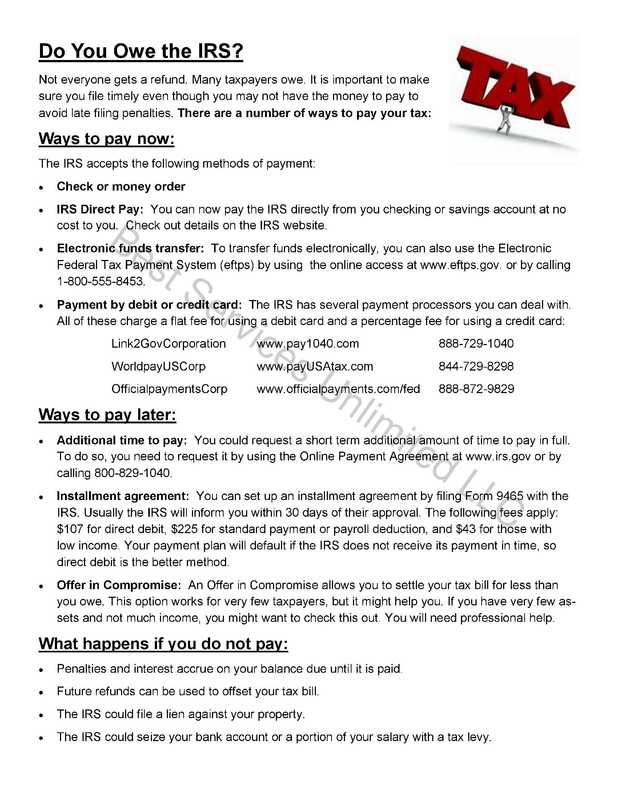

|

|

|

On April 26, 2017, with some fanfare, the Trump administration has provided information on proposed tax law changes, many of which mirror his previous tax policy statements. Although these proposals lack significant detail, here is what the president proposes and how it might impact your tax liability:

Business Tax Rates: Trump’s proposal would cut the top rate on corporate taxable income from 35% to 15%. Presumably, the 15% rate would apply to all business income, including small family-owned businesses. Individual Tax Rates – Under Trump’s proposal, there would only be three tax brackets, 10, 25, and 35%, down from the current seven tax brackets: 10, 15, 25, 28, 33, 35 and 39.6%. The brackets are applied in steps, so as a taxpayer’s income increases the increase is taxed at increasingly higher rates. The current proposal generally mirrors the rates Trump proposed while on the campaign trail. Under the previous proposal, for married taxpayers filing jointly, the lowest rate would apply to income less than $75,000; the 25% rate would apply to income more than $75,000 but less than $225,000; and the 33% rate would apply to income of more than $225,000. Brackets for single filers were 1/2 of joint filer amounts. However, the income brackets where the rates apply have not been specified in the current proposal and are subject to negotiations with Congress. Regardless, the reduction of the top tax rate from 39.6% to 35% will provide a huge tax saving for wealthy taxpayers. Standard Deduction – Trump originally suggested a standard deduction of $25,000 for singles and $50,000 for married couples. He has since toned that down and is now proposing to double the standard deduction, which is currently (2016) $12,600 for a married couple filing jointly and $6,300 for single taxpayers. Under Trump’s proposal the standard deductions would increase to approximately $24,000 for married couples and $12,000 for single taxpayers. According to an estimate by the nonpartisan Tax Policy Center (TPC), 27 million (60%) of the 45 million filers who would otherwise itemize in 2017 would opt for the standard deduction. This change would generally provide a small tax benefit to lower-income taxpayers. Itemized Deductions – During the campaign, Trump proposed limiting itemized deductions to $100,000 for single filers and $200,000 for joint filers, which would cause an increase in taxes for the wealthiest taxpayers and not impact middle-income taxpayers. However, the current proposal would do away with all itemized deductions except those that incentivize home ownership and charitable deductions. The theory is that the other deductions primarily benefit the wealthiest taxpayers. However, this would also have a significant impact on other taxpayers as well. Here are a few examples of its effects:

Other Deductions – Under the Trump proposal, virtually all deductions other than retirement savings would be eliminated. If that is the plan, then presumably it would include moving deductions, educators’ expenses, self-employed health insurance, student loan interest, and alimony paid. None of these changes would provide any significant benefit to the wealthy but would impact lower-income taxpayers. Alternative Minimum Tax (AMT) – Trump would eliminate the AMT, which primarily impacts wealthier taxpayers. Estate Tax – The proposal would also eliminate the estate tax, which applies to wealthy taxpayers with taxable estates in excess of $5,450,000 (2016). The number of taxable estates in the U.S. per year is just over 10,000. This proposal was presented as a one-page outline without any fundamental details. Assuming the proposal is not dead on arrival, expect significant changes to be made by Congress. For instance, the senators and representatives from states with income tax will certainly want to retain state income tax as an itemized deduction for their constituents, including both Democrats and Republicans. And of course, there needs to be replacement revenue for the cuts to avoid a national debt increase. As the tax reform debate winds through Washington, rest assured we will stay on top of the latest proposals and final legislation. We will continue to keep you informed during this wild ride.

0 Comments

Starting a new business is one of life's most exciting adventures. However, in order to build a successful company you need to start turning a profit as soon as possible. In the beginning of any business, expenses are unavoidable, but you can increase your profits by minimizing these expenses as much as possible. Here are eight tips you can use to save money while building your startup company.

1. Be careful with perks. As a new business, you want to attract the best employees to your company. However, trying to offer the same perks as a venture capital startup can put you in debt quickly. Many successful businesses started in a garage, and there is no shame in keeping things simple at first. Once you've made it, you can start thinking about adding cappuccino machines, ping pong tables, and other perks to your office environment. 2. Use free software programs. As you begin building your new business, resist the urge to invest in the latest, most expensive software programs. Instead, look for inexpensive software programs, or find programs that offer a lengthy free trial period. For example, instead of investing in Microsoft Office, you may consider using the free software programs offered by Google or Trello. 3. Make the most of your credit cards. If you already have credit cards, make sure you are getting the most out of any perks they offer, such as frequent flyer miles or cash back. If you are planning to apply for a business credit card, research your options carefully, and choose the card that will give you the best benefits. 4. Hire interns from local colleges. Instead of looking to the open market to find all of your employees, consider hiring interns from a local college instead. These individuals work for much less than a seasoned professional would, and they are often eager to prove themselves in the workplace. 5. Barter for services. As you work to grow your business, you may need a variety of services from independent contractors or other companies. Instead of offering to pay cash for the services you receive, try to offer a different type of benefit that won't impact your bottom line as much. For example, you may offer some of your own products or services, or you may allow the other party to collect a small amount of the profits you earn because of their services. 6. Minimize your personal expenses. Because you will likely be investing a lot of your own money into your startup, you can increase profitability by reducing your personal expenses. Be careful about how you spend money, especially when you start bringing in revenue. Avoid making large purchases, such as a new house or car, unless they are absolutely necessary. Consider working with your accountant to keep track of all of your expenses so you can identify opportunities to cut back. 7. Outsource some of your projects. To save more money while your business is getting off the ground, consider outsourcing some of your smaller projects, such as building or updating your website. Outsourcing one-time projects to independent contractors or consulting companies can be much more cost-effective than trying to hire a full-time employee to handle the job. 8. Use LinkedIn for recruitment. Recruiting new employees can be expensive, especially if you are determined to find the best people. To cut down on these costs, consider using LinkedIn to recruit new people for your startup. Although you will have to do some of the legwork, you won't spend as much as you would with other recruiting strategies. Regardless of the steps you take to save money as your business grows, you will still need to manage your funds carefully to ensure that your financial situation is improving over time. A professional accountant can help you set up a realistic budget and cash flow forecast to keep you on the right track. Need a business plan, we can help with that too. Contact our office today at (770) 829-0082 to learn more. |

Archives

December 2017

Categories |

RSS Feed

RSS Feed