|

|

|

As Tax Season 2018, approaches most people are getting prepared to take their tax documents to the same tax professional believing they are getting the best service and maximizing your tax refund.

However, what has your tax professional done to ensure he/she is ready for Tax Season 2018? Whether a tax preparer, enrolled agent, tax accountant, or CPA, yearly continuing education is necessary to stay abreast of the ever-changing tax laws. Here are some questions you need to ask to ensure you are getting the best service and maximizing your tax refund.

Asking your tax professional questions is your right. Verify credentials, it's important to know your information is in the hands of a reputable and honest tax professional. Nine out of ten if your tax professional cannot answer these simple questions, they cannot offer you the best service or maximizing your tax refund.

0 Comments

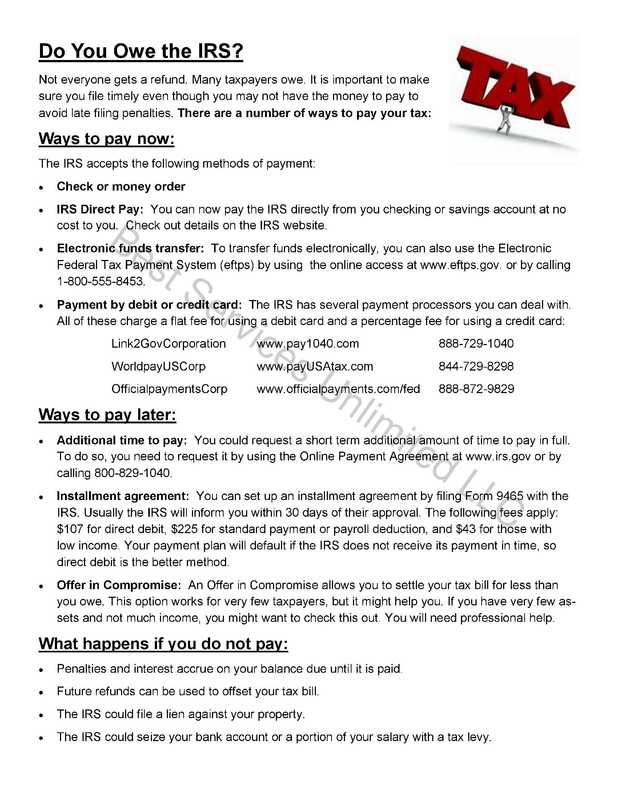

Monday is October 16th and frantic tax filers of late returns will be looking for any means possible to pay less to Uncle Sam.

The following tips should help you file your return and officially close this tax reporting year:

Your year-end tax planning can be extremely important when tax season rolls around. When you’re setting up your tax planning before year-end, be sure to include these two things to help lower your 2017 tax bill.

Open an HSA If, like most self-employed people, you pay for your own health insurance, consider opening a Health Savings Account (HSA). An HSA is like a health IRA that is coupled with a health insurance policy with a high deductible. You can deduct contributions to your HSA and then use the money to pay almost any uninsured health-related expense. And you don’t have to pay any taxes on these withdrawals. For 2017, individuals can contribute up to $3,400 and family plans up to $6,750 to their HSAs (people over 55 can contribute $1,000 extra). If you set up your HSA and contribute by December 31, 2017, you can make a full year’s worth of deductible HSA contributions for 2017. Donate to Charity If you itemize your deductions, you’ll lower your 2017 income taxes by donating to charity by the end of the year. You can donate money, property, or both, to any qualified charity and take a deduction. If a charity has obtained a determination letter from the IRS recognizing its status as a 501(c)(3) public charity, then it is qualified for tax purposes and donations to it are deductible. Many nonprofits include copies of their IRS determination letter on their website and their taxpayer identification number on fundraising solicitations so donors know they can deduct donations to their organization. The only 501(c)(3) organizations that are automatically considered qualified organizations (without a determination letter from the IRS) are churches and other religious organizations. Make sure to keep records of all your donations. The IRS maintains a database of qualified organizations, which is available to the public on its website. Other organizations maintain even more extensive lists of nonprofits. For example, the website GuideStar lists over 1.5 million nonprofits. For more tax tips like these, download a copy of our year-end tax savings newsletter.  Currently, IRS guidelines only allow you to get an IP PIN if you filed last year's return with a home address in Florida, Georgia or Washington, D.C., Or if the IRS invites you to apply, which generally only happens if you have already been a victim of tax-related identity theft.

WHAT TO DO

ON MY SOAPBOX Equifax you messed up big-time and you need to work with the IRS to issue everyone affected with a IRS IP PIN before year-end to get ahead of the crooks. It's the best thing to do to protect all taxpayers from tax fraud. Please implement these strategies and protect your tax return and credit NOW!! #ProtectYourTaxReturn #IamYvetteDBest #ThePeoplesTaxAccountant  Article Highlights:

With the historic flooding and damage caused by recent hurricanes, President Trump has declared the affected areas disaster areas. If you were an unlucky victim and suffered a loss as a result of these disasters, you may be able to recoup a portion of that loss through a tax deduction. When you suffer a casualty loss within a federally declared disaster, you can elect to claim the loss in one of two years: the tax year in which the loss occurred or the immediately preceding year. Income Tax Casualty Loss - By taking the deduction for a 2017 disaster area loss on the prior year (2016) return, you may be able to get a refund from the IRS before you even file your tax return for 2017, the loss year. You have until six months after the original due date of the 2017 return to make the election to claim it on your 2016 return, in most cases by filing an amended 2016 return to claim the disaster loss. Before making the decision to claim the loss in 2016, you should consider which year’s return would produce the greater tax benefit, as opposed to your desire for a quicker refund. If you elect to claim the loss on either your 2016 original or amended return, you can generally expect to receive the refund within a matter of weeks, which can help to pay some of your repair costs. If the casualty loss, net of insurance reimbursement, is extensive enough to offset all of the income on the return, whether the loss is claimed on the 2016 or 2017 return, and results in negative income, you may have what is referred to as a net operating loss (NOL). When there is an NOL, the unused loss can be carried back two years and then carried forward until it is all used up (but not more than 20 years), or you can elect to only carry the unused loss forward. Determining the more beneficial year in which to claim the loss requires a careful evaluation of your entire tax picture for both years, including filing status, amount of income and other deductions, and the applicable tax rates. The analysis should also consider the effect of a potential NOL. Ordinarily, casualty losses are deductible only to the extent they exceed $100 plus 10% of your adjusted gross income (AGI). Thus, a year with a larger amount of AGI will cut into your allowable loss deduction and can be a factor when choosing which year to claim the loss. For verification purposes, keep copies of local newspaper articles and/or photos that will help prove that your loss was caused by the specific disaster. As strange as it may seem, a casualty might actually result in a gain. This sometimes occurs when insurance proceeds exceed the tax basis of the destroyed property. When a gain materializes, there are ways to exclude or postpone the tax on the gain. Extension of Filing and Payment Due Dates The IRS has announced that Hurricane Harvey and Irma victims have until Jan. 31, 2018, to file certain individual and business tax returns and make certain tax payments. This tax relief postpones various tax filing and payment deadlines that occurred starting on:

As a result, affected individuals and businesses will have until Jan. 31, 2018, to file returns and pay any taxes that were originally due during this period. This includes:

The IRS automatically provides filing and penalty relief to any taxpayer with an IRS address of record located in a disaster area. Thus, taxpayers need not contact the IRS to get this relief. However, if an affected taxpayer receives a late filing or late payment penalty notice from the IRS that has an original or extended filing, payment or deposit due date falling within the postponement period, the taxpayer should call the number on the notice to have the penalty abated. In addition, the IRS will work with any taxpayer who lives outside of a disaster area but whose records necessary to meet a deadline occurring during the postponement period are located in the affected area. Taxpayers qualifying for relief who live outside the disaster area need to contact the IRS at 866-562-5227. This also includes workers assisting the relief activities who are affiliated with a recognized government or philanthropic organization. The tax relief is part of a coordinated federal response to the damage caused by severe storms and flooding and is based on local damage assessments by FEMA. For information on disaster recovery, visit disasterassistance.gov. For information on government-wide efforts related to:

If you need further information on filing extensions, casualty and disaster losses, your particular options for claiming a loss, or if you wish to amend your 2016 return to claim your 2017 loss, please give this office a call at (770) 829-0082.  The reason withdrawals from an Individual Retirement Account (IRA) prior to age 59½ are generally subject to a 10% tax penalty is that policymakers wanted to create a disincentive to use these savings for anything other than retirement.¹

Yet, policymakers also recognize that life can present more pressing circumstances that require access to these savings. In appreciation of this, the list of withdrawals that may be taken from an IRA without incurring a 10% early withdrawal penalty has grown over the years. Penalty-Free WithdrawalsOutlined below are the circumstances under which individuals may withdraw from an IRA prior to age 59½, without a tax penalty. Ordinary income tax, however, generally is due on such distributions.

Wedding bells will soon be heard in the air! June followed by September and October are the most common months to get married. However, in tax law, if you are married by the end of the year, you are considered married for the entire year. This is just one of the changes. Marriage can make more changes in your tax situation, some good, and some bad.

Some more of the changes are listed below. These also apply to same-sex marriages. Change in Filing Status:

Name Change If your name changes with marriage, you should contact Social Security. The IRS uses records from Social Security to cross check Social Security numbers with names. It would be wise to file Form SS-5 (application for a Social Security card) to correct the situation. Your Social Security number will remain the same. Address Change You should file Form 8822 with the IRS. Circumstance Change If you purchased health insurance through the Health Insurance Marketplace, you could have a change in your premium credit. Reporting the change could avoid a tax surprise. Withholding Change Your current withholding on your job as a single person is higher than the married rate. The married withholding tax tables were set in place during a time when families had one-wage earner. Now it’s more common for both to work. The married tax tables work great for the one earner family, but it wise to use single tax tables, if both of you work. Need Help? Feeling Overwhelmed? Trust, there's a much easier way to officially change your name. You can use Hitchswitch Name Change and choose the package you want, and everything will be changed in 3 steps. It takes all of the guess and legwork out of the process. This service is so worth it, especially since all you have to do is fill out 1 single form. It doesn't get simpler than that!  On April 26, 2017, with some fanfare, the Trump administration has provided information on proposed tax law changes, many of which mirror his previous tax policy statements. Although these proposals lack significant detail, here is what the president proposes and how it might impact your tax liability:

Business Tax Rates: Trump’s proposal would cut the top rate on corporate taxable income from 35% to 15%. Presumably, the 15% rate would apply to all business income, including small family-owned businesses. Individual Tax Rates – Under Trump’s proposal, there would only be three tax brackets, 10, 25, and 35%, down from the current seven tax brackets: 10, 15, 25, 28, 33, 35 and 39.6%. The brackets are applied in steps, so as a taxpayer’s income increases the increase is taxed at increasingly higher rates. The current proposal generally mirrors the rates Trump proposed while on the campaign trail. Under the previous proposal, for married taxpayers filing jointly, the lowest rate would apply to income less than $75,000; the 25% rate would apply to income more than $75,000 but less than $225,000; and the 33% rate would apply to income of more than $225,000. Brackets for single filers were 1/2 of joint filer amounts. However, the income brackets where the rates apply have not been specified in the current proposal and are subject to negotiations with Congress. Regardless, the reduction of the top tax rate from 39.6% to 35% will provide a huge tax saving for wealthy taxpayers. Standard Deduction – Trump originally suggested a standard deduction of $25,000 for singles and $50,000 for married couples. He has since toned that down and is now proposing to double the standard deduction, which is currently (2016) $12,600 for a married couple filing jointly and $6,300 for single taxpayers. Under Trump’s proposal the standard deductions would increase to approximately $24,000 for married couples and $12,000 for single taxpayers. According to an estimate by the nonpartisan Tax Policy Center (TPC), 27 million (60%) of the 45 million filers who would otherwise itemize in 2017 would opt for the standard deduction. This change would generally provide a small tax benefit to lower-income taxpayers. Itemized Deductions – During the campaign, Trump proposed limiting itemized deductions to $100,000 for single filers and $200,000 for joint filers, which would cause an increase in taxes for the wealthiest taxpayers and not impact middle-income taxpayers. However, the current proposal would do away with all itemized deductions except those that incentivize home ownership and charitable deductions. The theory is that the other deductions primarily benefit the wealthiest taxpayers. However, this would also have a significant impact on other taxpayers as well. Here are a few examples of its effects:

Other Deductions – Under the Trump proposal, virtually all deductions other than retirement savings would be eliminated. If that is the plan, then presumably it would include moving deductions, educators’ expenses, self-employed health insurance, student loan interest, and alimony paid. None of these changes would provide any significant benefit to the wealthy but would impact lower-income taxpayers. Alternative Minimum Tax (AMT) – Trump would eliminate the AMT, which primarily impacts wealthier taxpayers. Estate Tax – The proposal would also eliminate the estate tax, which applies to wealthy taxpayers with taxable estates in excess of $5,450,000 (2016). The number of taxable estates in the U.S. per year is just over 10,000. This proposal was presented as a one-page outline without any fundamental details. Assuming the proposal is not dead on arrival, expect significant changes to be made by Congress. For instance, the senators and representatives from states with income tax will certainly want to retain state income tax as an itemized deduction for their constituents, including both Democrats and Republicans. And of course, there needs to be replacement revenue for the cuts to avoid a national debt increase. As the tax reform debate winds through Washington, rest assured we will stay on top of the latest proposals and final legislation. We will continue to keep you informed during this wild ride.  Starting a new business is one of life's most exciting adventures. However, in order to build a successful company you need to start turning a profit as soon as possible. In the beginning of any business, expenses are unavoidable, but you can increase your profits by minimizing these expenses as much as possible. Here are eight tips you can use to save money while building your startup company.

1. Be careful with perks. As a new business, you want to attract the best employees to your company. However, trying to offer the same perks as a venture capital startup can put you in debt quickly. Many successful businesses started in a garage, and there is no shame in keeping things simple at first. Once you've made it, you can start thinking about adding cappuccino machines, ping pong tables, and other perks to your office environment. 2. Use free software programs. As you begin building your new business, resist the urge to invest in the latest, most expensive software programs. Instead, look for inexpensive software programs, or find programs that offer a lengthy free trial period. For example, instead of investing in Microsoft Office, you may consider using the free software programs offered by Google or Trello. 3. Make the most of your credit cards. If you already have credit cards, make sure you are getting the most out of any perks they offer, such as frequent flyer miles or cash back. If you are planning to apply for a business credit card, research your options carefully, and choose the card that will give you the best benefits. 4. Hire interns from local colleges. Instead of looking to the open market to find all of your employees, consider hiring interns from a local college instead. These individuals work for much less than a seasoned professional would, and they are often eager to prove themselves in the workplace. 5. Barter for services. As you work to grow your business, you may need a variety of services from independent contractors or other companies. Instead of offering to pay cash for the services you receive, try to offer a different type of benefit that won't impact your bottom line as much. For example, you may offer some of your own products or services, or you may allow the other party to collect a small amount of the profits you earn because of their services. 6. Minimize your personal expenses. Because you will likely be investing a lot of your own money into your startup, you can increase profitability by reducing your personal expenses. Be careful about how you spend money, especially when you start bringing in revenue. Avoid making large purchases, such as a new house or car, unless they are absolutely necessary. Consider working with your accountant to keep track of all of your expenses so you can identify opportunities to cut back. 7. Outsource some of your projects. To save more money while your business is getting off the ground, consider outsourcing some of your smaller projects, such as building or updating your website. Outsourcing one-time projects to independent contractors or consulting companies can be much more cost-effective than trying to hire a full-time employee to handle the job. 8. Use LinkedIn for recruitment. Recruiting new employees can be expensive, especially if you are determined to find the best people. To cut down on these costs, consider using LinkedIn to recruit new people for your startup. Although you will have to do some of the legwork, you won't spend as much as you would with other recruiting strategies. Regardless of the steps you take to save money as your business grows, you will still need to manage your funds carefully to ensure that your financial situation is improving over time. A professional accountant can help you set up a realistic budget and cash flow forecast to keep you on the right track. Need a business plan, we can help with that too. Contact our office today at (770) 829-0082 to learn more. |

Archives

December 2017

Categories |

RSS Feed

RSS Feed